at Next Market Open

Set Trade Exits:

Model Scores below are for reference only. Trades are made on today's signal (top left), which is a composite of the two models scores below.

4/27/2025

4/26/2025

4/25/2025

4/24/2025

4/23/2025

90

82

77

76

65

Several trend, momentum, and volatility measures are aligned constructively. APAC and credit markets healthy.

4/27/2025

4/26/2025

4/25/2025

4/24/2025

4/23/2025

90

82

77

76

65

200-day trend/RSI look supportive and volatility signals are too mild to trigger the crash filter.

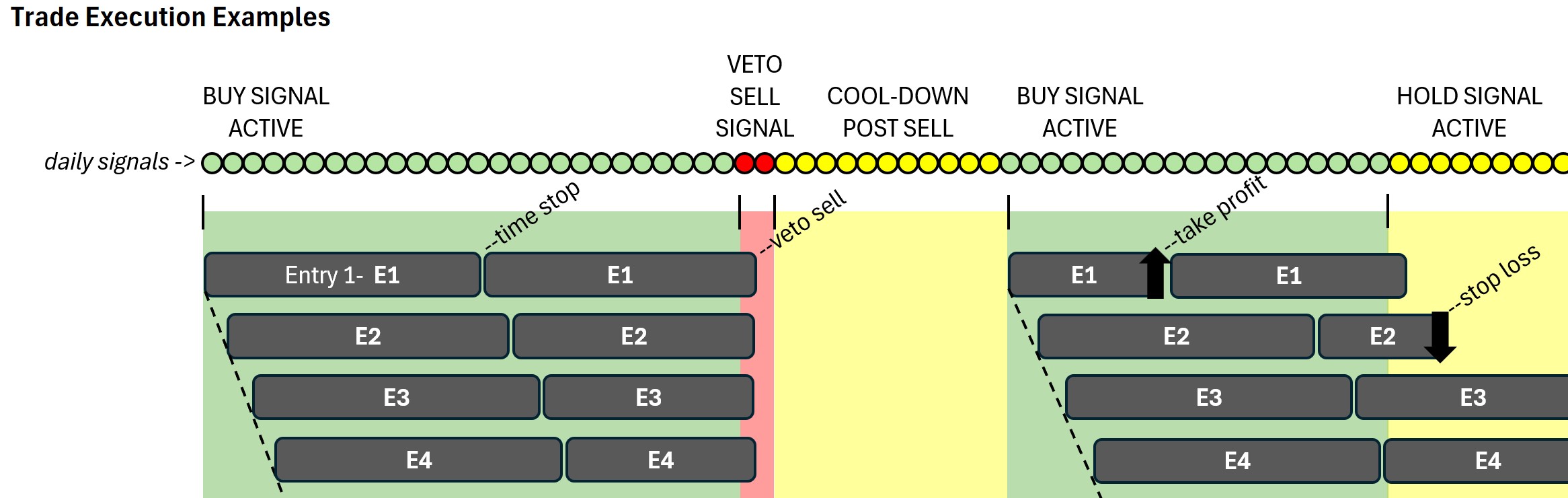

Benchmark3x is rules-based and probabilistic. To reduce entry-timing risk, split your total intended investment position into 4 to 5 equal entries and deploy them in a staggered sequence as shown below. This reduces entry-risk, smooths out volatility and aligns your returns with the model's long-term average.

BUY (Green) signal: Buy at the next market open. Add up to one entry per day until fully allocated.

HOLD (Yellow): No new entries. Maintain current positions. Only sell if a stop loss, take profit, or max time in trade is reached.

SELL / VETO (Red): Exit all entries at the next market open. A cooldown period then blocks new entries for a period of time.

The graphic below shows a sample execution flow and the four possible exits: Time Stop, Veto Sell, Take Profit, Stop Loss.

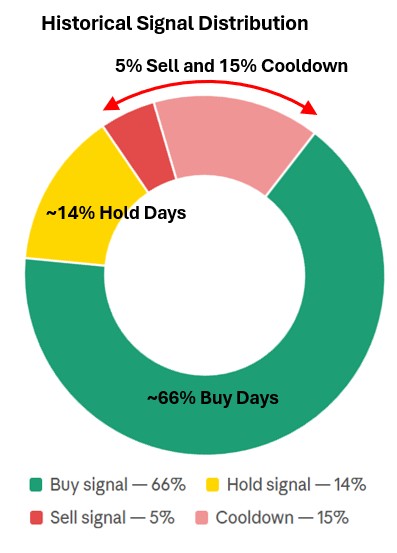

This Historical Signal Distribution chart shows the approximate share of market days spent in each Benchmark3x signal state.

Most days have been Buy days (~66%), meaning the model recommends getting into the market on a significant majority of days.

A smaller portion of days fall into Hold (~14%), where no new entries are added but existing positions are maintained.

Sell days have been relatively rare (~5%), while Cooldown reflects the period after a sell signal when new entries are temporarily blocked.